Housing affordability is at its worst level in decades, and it is more challenging than ever for first-home buyers to get their feet on the property ladder.

According to PropTrack's Housing Affordability Report, dramatic mortgage rate increases and rising home prices have meant that property seekers in 2023 can afford fewer homes than when records began in 1995.

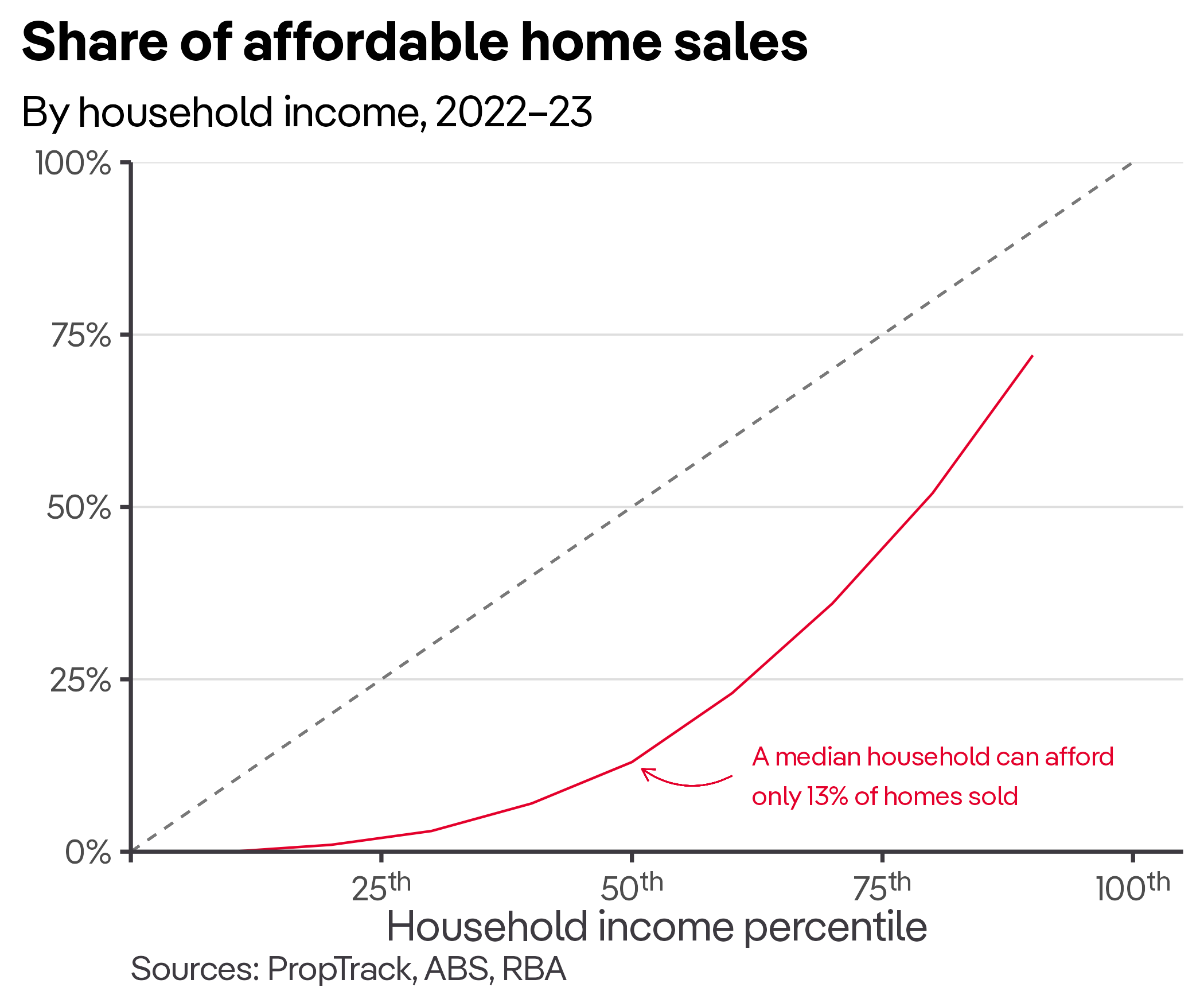

For example, households earning the median (or typical) income in Australia can afford just 13% of homes sold nationwide.

This is a significant fall from the peak affordability levels in 2019-20 and 2020-21 when a median-income household could afford nearly 40% of homes sold across Australia.

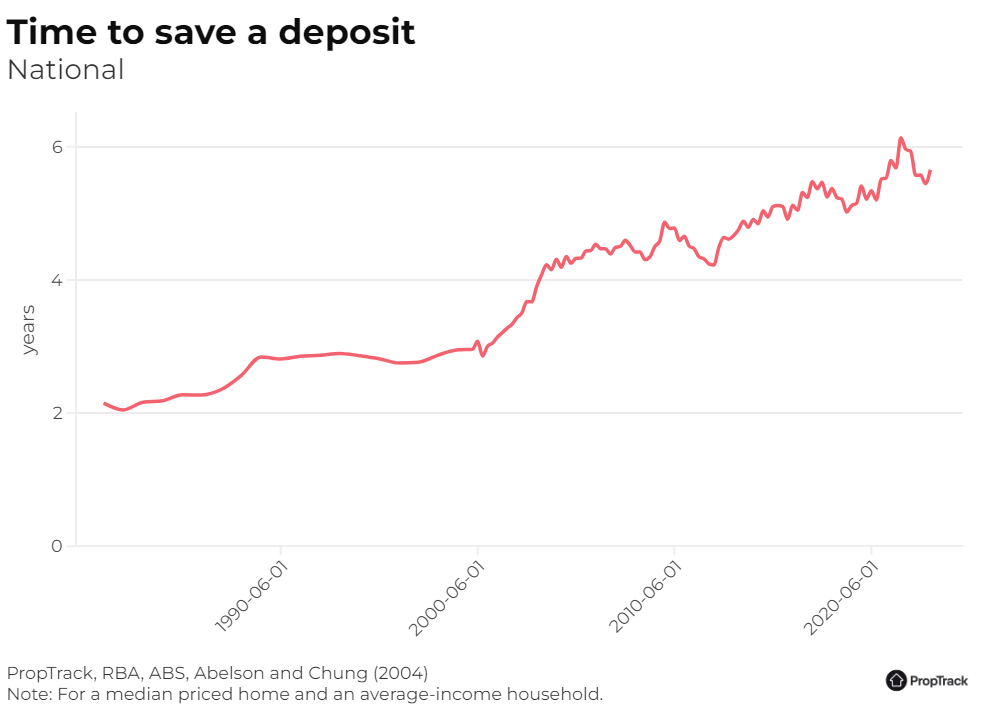

Being able to pay the mortgage is just one part of the puzzle; the second is having enough savings for a deposit.

Most mortgage lenders require a 20% deposit, otherwise, borrowers will be subject to higher interest rates and must pay mortgage lender's insurance (LMI).

The time needed to save a deposit is calculated as the number of years a household earning average household income would need to save 20% of their gross household income to accumulate a 20% deposit on a median-priced home.

An average-income household would need to save 20% of their income for more than five and a half years to save a 20% deposit on a median-priced home.

Currently, the median property price in Australia is $678,500, which would mean saving $135,700 to avoid a higher mortgage rate and paying LMI.

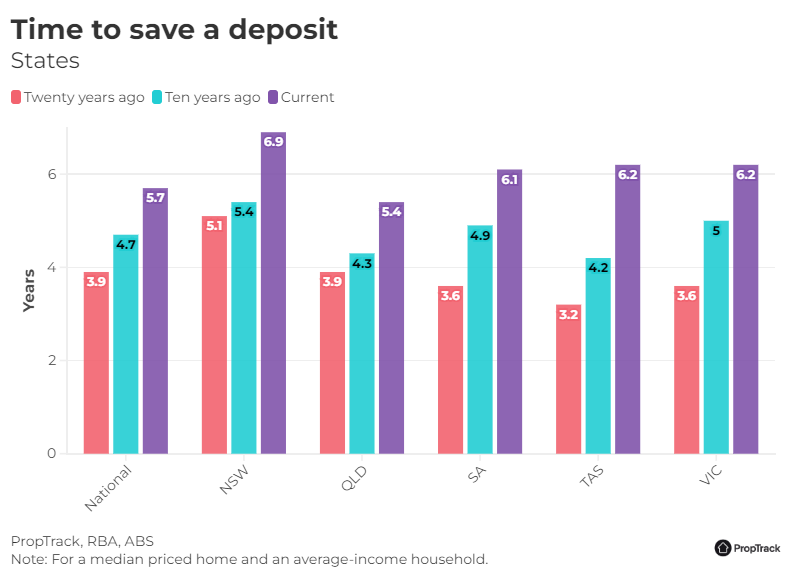

Unfortunately, there are states where the median-priced home and average income make it even harder to save for a home.

In New South Wales, it would take an average household nearly seven years to save a 20% deposit for a median-priced home. Ten years ago, it was five and a half years.

The median price in NSW is $860,000, 20% of which is $172,000.

Victoria and Tasmania have the second highest time to save a deposit, at just over six years.

If you live in Queensland, the outlook is slightly better. An average household on a median income could have enough for a deposit in 5.4 years.

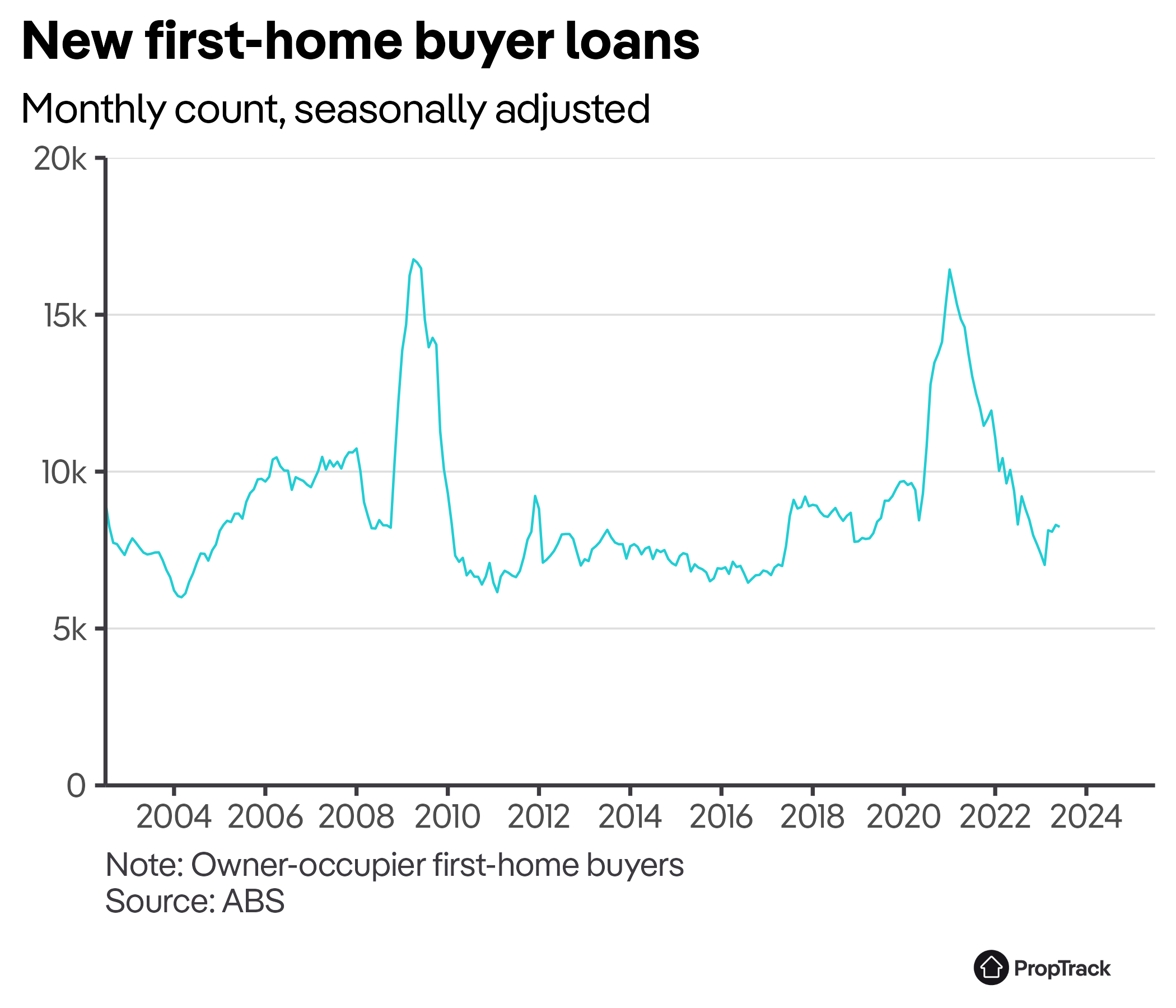

For many first-home buyers, the combination of record low interest rates and government incentives made 2020 and 2021 favourable times to buy.

Throughout 2021, more than 160,000 first-home buyers took out new mortgages, the highest annual number in over a decade.

Since this peak, loans to first-home buyers have plummeted, driven by increasing interest rates making it harder to afford a mortgage.

In recent months, more first-home buyers have rejoined the market; however, these numbers are still historically very low.

With expectations that interest rates are at, or close to their peak, and employment and wages growth likely to continue, the dramatic decline in affordability starting in late 2021 may begin to slow.

However, affordability will continue to be an issue in Australia for the foreseeable future, especially as home prices continue to rise.